Where to Sell Audiobooks in 2025: Audible, Spotify, Apple—and Going Wide with PublishDrive

Last month, I was reviewing our distribution data across platforms when something caught my attention: publishers using PublishDrive who distributed audiobooks to at least 5 platforms earned 2.3x more than those going exclusive to a single retailer.

Not 10% more. Not 20% more. 2.3 times more revenue.

This isn't just a PublishDrive phenomenon—it's what's happening across the entire audiobook market in 2025. And if you're still debating whether to go exclusive or wide, the data has already made that decision for you.

Let me show you where audiobooks are selling, why the landscape just fundamentally changed, and how to capture revenue you're currently leaving on the table.

Retail vs. Subscription: Understanding the New Audiobook Economy

The audiobook marketplace isn't one market anymore—it's multiple parallel ecosystems operating under completely different economics:

The Retail Model (Transaction-Based):

- Listeners purchase individual audiobooks outright

- Higher per-unit revenue for publishers

- Discovery happens through browsing, recommendations, bestseller lists

- Examples: Apple Books, Google Play Books, Kobo Audiobooks

The Subscription Model (Access-Based):

- Listeners pay monthly fees for unlimited or credit-based listening

- Revenue comes from per-listen royalties or credit redemptions

- Discovery happens through algorithmic recommendations and curated collections

- Examples: Audible Plus, Spotify Audiobooks, Scribd, Elevenlabs

PublishDrive's data shows that 19% of all audiobook sales came from pure subscription-based business models, where publishers are remunerated through a subscription pool model rather than individual sale prices. However, more than 70% of audiobook sales were generated in stores offering subscription services to listeners, meaning listeners pay a monthly fee instead of purchasing books individually. The market clearly prefers subscription services, but publishers need remuneration packages that still value their contracts with authors and copyright holders while covering their costs.

Here's what most publishers miss: these aren't competing models—they're complementary audiences.

Retail buyers are intentional purchasers who know what they want. Subscription listeners are explorers willing to try new authors because the psychological friction of "spending $20" disappears inside an all-you-can-consume model.

You need both.

The Library Model (Access and Transaction-Based)

There's a third economic model that most publishers overlook entirely—and it's one of the most stable revenue streams in audiobook distribution:

The Library Lending Model:

- Libraries purchase audiobooks for their digital collections

- Patrons borrow audiobooks through apps like Libby (powered by OverDrive)

- Publishers earn revenue through institutional purchases and circulation-based royalties

- Hybrid model: Libraries pay for access, individual listeners borrow for free

OverDrive, a key library partner of PublishDrive, contributed 16% to total audiobook sales in 2024, tripling its growth compared to the previous year through PublishDrive. OverDrive’s top markets are the English speaking markets, particularly the US, Australia, Canada, the UK, New Zealand. The integration of Kindle Unlimited with library distribution, which will no longer penalize authors for publishing in libraries, is expected to significantly boost the relevance of library distribution across all formats in 2026.

Why libraries matter more than you think:

- Different demographic reach:

- Budget-conscious listeners who can't afford $20+ audiobooks regularly

- Voracious readers consuming 11-12 books monthly (they need a cost-effective way to feed that habit)

- Older demographics (55+) more comfortable with library systems than subscription apps

- Students and educators with institutional access

- Rural and underserved communities with limited bookstore access

- Discovery funnel for retail conversion: The typical pattern we see: A reader discovers your audiobook through library lending, loves it, then purchases your entire backlist on Apple Books or Audible because they want to own the series permanently and support the author.

- Consistent backlist revenue: Unlike retail, where titles typically see 80% of lifetime sales in the first 90 days, library lending generates steady, predictable revenue for years. Libraries maintain standing orders, and circulation-based royalty models mean older titles continue earning as long as patrons keep borrowing them.

- Institutional stability: While individual consumer behavior can be volatile (remember BookTok's 4.5% sales dip in July 2023?), library budgets and purchasing patterns remain relatively stable year-over-year.

The strategic mistake: Going exclusive to one retailer means libraries can't purchase your audiobooks. You're eliminating an entire revenue stream and a critical discovery channel that disproportionately benefits backlist titles.

The opportunity: Publishers distributing to OverDrive alongside retail and subscription platforms capture three distinct audience segments: intentional retail buyers, exploratory subscription listeners, and budget-conscious library patrons who often become your most loyal fans.

Audible's Role: The 800-Pound Gorilla You Can't Ignore

Let's address this directly: Audible dominates the US audiobook market. Within PublishDrive's network, Audible consistently ranks as one of the fastest-growing platforms for our publishers' audiobook sales with 5x growth in 2024 compared to previous year.

That dominance creates a temptation: go exclusive to Audible Plus (their subscription tier), accept their terms, and focus your energy there.

Here's why that's a mistake:

What Audible Plus exclusivity gets you:

- Access to Audible's massive listener base

- Potential promotional placement

- Higher royalty rates within Audible's ecosystem

What Audible exclusivity costs you:

- 30% of your potential international audience (our data—remember that number)

- Zero presence on Apple Books (the second-largest audiobook retailer)

- No access to Spotify's 615 million users discovering audiobooks for the first time

- Elimination from library lending platforms reaching different demographics

- Complete dependence on one company's algorithm and promotional decisions

Audible is essential. Audible exclusivity is expensive.

The publishers seeing 2.3x revenue growth in our network? They're on Audible and everywhere else.

Spotify's Discovery Effect: Why Streaming Changed Everything

This is the part that makes me excited about where audiobooks are headed.

Spotify launched audiobooks in late 2023, and what we're seeing in 2024-2025 isn't just another platform entering the market—it's a fundamental shift in who discovers audiobooks and how.

Here's the dynamic most publishers are missing:

Spotify has 615 million active users who already engage with audio content daily. These aren't necessarily book buyers. Many aren't traditional readers at all. But they're comfortable with streaming. They're accustomed to algorithmic discovery. They trust Spotify's recommendations.

And now, those recommendations include audiobooks.

The psychology is powerful: "I'm already paying for Spotify Premium. I get 15 hours of audiobooks included. I might as well try something new."

That "might as well try something new" behavior? It disproportionately benefits:

- Debut authors without established platforms

- Backlist titles that would never get promotional placement

- Genre fiction that thrives on binge-listening behavior

- International authors reaching English-language audiences

If you're not on Spotify, you're invisible to the fastest-growing segment of audiobook listeners—people who didn't think of themselves as "audiobook people" until streaming made it frictionless.

Apple, Google, Kobo: The High-Intent Retail Buyers

While subscription platforms capture exploratory listeners, the retail platforms serve a different, equally valuable audience: high-intent buyers who want to own audiobooks permanently.

Apple Books remains the second-largest audiobook retailer globally and consistently performs well within PublishDrive's distribution network. Apple's ecosystem integration—seamless syncing across iPhone, iPad, Mac, and CarPlay—creates a premium listening experience that commands premium pricing.

Apple Books is one of the best performing audiobook store in PublishDrive’s network selling a lot in fantasy, business, self-help and health and fitness in audiobooks in 2024.

Our data shows Apple Books performs particularly well for:

- Premium fiction with professional narration

- Non-fiction in business, self-help, and personal development

- Authors with existing Apple ecosystem brand loyalty

Google Play Books serves Android's massive global market, with particularly strong performance in international territories. The platform's integration with Google Assistant and Android Auto mirrors Apple's ecosystem advantages.

Google Play Books sell fantasy, romance, self-help, thrillers and business books a lot in audiobooks more than doubling its performance compared to last year same period. 64% of overall sales came from the US market, meanwhile 36% of it came from international markets that is higher than in our general audiobook trends.

Kobo Audiobooks may have smaller overall market share, but it serves a fiercely loyal reader base—often book enthusiasts who deliberately choose not to use Amazon. Our publishers report that Kobo listeners tend to be voracious consumers with high lifetime value.

Kobo audiobooks were showing a particular 3x growth in Canada showcasing its strong international presence outside of the US.

The critical insight: Each platform attracts subtly different listener demographics. By distributing wide, you're not just increasing volume—you're accessing distinct audience segments that would never discover you on a single platform.

Why Wide Distribution Wins (The Data You Need to See)

Let me show you exactly why the "wide vs. exclusive" debate is over.

PublishDrive's 2024 distribution data:

For US-based publishers using our platform, 30% of their audiobook sales came from outside the United States. The top international markets included the UK, Australia, Denmark, Canada, Sweden, Norway, the Netherlands, Germany, Finland, Ireland, and New Zealand.

Let that sink in: If you're distributing exclusively through one US-focused retailer, you're potentially missing 30% of your audience.

But the international story is only part of it. Even within the US market, we see clear patterns:

Publishers distributing to 5+ platforms averaged 2.3x higher revenue than single-platform publishers, even when that single platform was a major retailer.

Why? Because different listeners have different platform preferences based on:

- Device ecosystems (Apple users default to Apple Books; Android users favor Google Play)

- Existing subscriptions (Spotify Premium members try audiobooks there first)

- Discovery habits (Audible browsers vs. library patrons vs. retail buyers)

- Price sensitivity (subscription listeners vs. ownership-minded purchasers)

You're not choosing between platforms. You're choosing whether to capture 100% of your potential audience or artificially limit yourself to 30-40% for no strategic benefit.

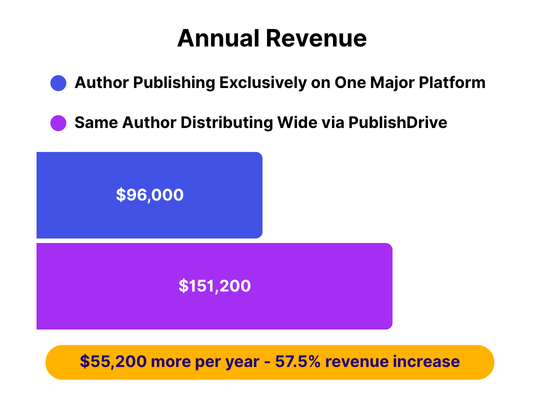

The Real Cost of Exclusivity

Let's do the math with a real scenario:

Author publishing exclusively on one major platform:

- 1,000 audiobook sales/month

- Average royalty: $8 per sale

- Monthly revenue: $8,000

- Annual revenue: $96,000

Same author distributing wide via PublishDrive:

- Primary platform: 700 sales (you lose some volume when not exclusive)

- Secondary retail platforms: 450 sales (Apple, Google, Kobo)

- Spotify (new discovery): 200 sales

- Library lending: 150 sales (steady backlist consumption)

- International markets: 300 sales (30% of total)

- Average royalty: $7 per sale (slightly lower due to subscription/library mix)

- Total monthly sales: 1,800

- Monthly revenue: $12,600

- Annual revenue: $151,200

Result: $55,200 more per year—a 57.5% revenue increase—just from distribution strategy.

One-Dashboard Distribution with PublishDrive: How to Actually Go Wide Without Losing Your Mind

Here's the objection I hear constantly: "Wide distribution sounds great, but I don't have time to manage 10+ retailer dashboards, each with different metadata requirements, reporting formats, and payment systems."

Fair. That would be a nightmare.

That's exactly why PublishDrive exists.

How our distribution infrastructure works:

- Upload once, distribute everywhere: You upload your audiobook file, metadata, and cover to PublishDrive's platform once. We handle distribution to:

- Audible

- Apple Books

- Google Play Books

- OverDrive (libraries)

- Kobo Audiobooks

- Spotify Audiobooks

- ElevenReader (AI-narrated audiobooks)

- Plus 140+ additional stores globally

PublishDrive streamlines distribution and publishing by fostering strong relationships with retailers, eliminating the need for publishers to navigate multiple self-service platforms for tasks like price updates or keyword changes. For audiobooks, authors report saving up to 30 minutes per book, per upload, per platform. This efficiency allows authors to maximize royalties by reaching wider audiences and frees up valuable time, which can then be dedicated to audience engagement or content creation, instead of administrative logistics.

- Unified metadata management: Update your book description, pricing, or categories in one place. Changes propagate to all platforms automatically. No logging into seven different dashboards to change one keyword.

- Consolidated reporting: View sales data, revenue, and performance metrics across all platforms in a single dashboard. Compare how your audiobook performs on Audible vs. Apple vs. Spotify in real-time.

PublishDrive publishers can save up to 15+ hours per month on reporting and sales analytics with built in tools and analytics functions and saving extra money on bank fees as one payment would go land in the bank account instead of 13 or more per month.

- Zero commission model: You keep 100% of your store royalties. We charge a predictable monthly subscription fee regardless of sales volume. As your revenue grows, your distribution costs don't.

For publishers earning over $1,000/month in royalties, this model saves 10-20% compared to commission-based aggregators while providing access to more platforms. Also, in terms of audiobooks, where usually margins are already lower, it makes a huge difference to save on commissions and maximize your royalties.

PublishDrive helps publishers maximize royalties by allowing them to retain 100% of store royalties, unlike traditional aggregators that typically take a 15% commission. This means a publisher generating $2,000 monthly can gain an additional $3,600 annually by choosing PublishDrive, enabling reinvestment for growth.

5. AI-powered optimization: Our tools analyze your sales data across platforms and recommend where to focus marketing efforts, which territories show highest growth, and what metadata adjustments might improve discoverability.

The Strategic Framework: Where to Prioritize (If You Must)

If you're just starting with audiobooks and can't launch on every platform simultaneously, here's the prioritization framework we can see work for many publishers:

Phase 1: Essential Foundation (Launch Day)

- Audible (largest market share, essential credibility)

- Apple Books (second-largest retailer, premium buyers)

- Google Play Books (Android ecosystem, international reach)

Phase 2: Discovery Expansion (Month 2-3)

- Spotify Audiobooks (discovery for non-traditional listeners)

- OverDrive (library lending, backlist revenue)

Phase 3: International Optimization (Month 4+)

- Kobo Audiobooks (loyal niche audience)

- Regional platforms based on your genre/audience data

- Platform-specific promotional opportunities

But here's the thing: with PublishDrive, you don't need phases. You can launch everywhere simultaneously on day one, because the operational complexity is handled for you.

The question isn't "Can I afford to go wide?" It's "Can I afford not to?"

What This Means for Your Strategy

The audiobook market just crossed a threshold. With Spotify's entry, subscription streaming psychology is now mainstream. With international markets growing faster than the US, global distribution is mandatory. With listeners consuming 11-12 books monthly, they're actively seeking new authors across multiple platforms.

The old calculus—"go exclusive for higher royalties and promotional support"—no longer reflects market reality.

The new calculus: Maximize discovery across every channel where your listeners already spend time, retain full control of your distribution strategy, and capture revenue from audiences that would never find you on a single platform.

Your Next Step

Going wide isn't complicated anymore. It's actually the simpler strategy—if you have the right infrastructure.

Set up wide audiobook distribution in minutes with PublishDrive:

- Create your free account at publishdrive.com

- Upload your audiobook files, metadata, and cover

- Select all distribution platforms (it's literally checkboxes)

- We handle the rest—approval, distribution, ongoing reporting

Zero commission. One dashboard. Every platform.

The readers consuming 11-12 audiobooks monthly are already listening on Audible, Spotify, Apple, Google, and library apps. The question is whether they're listening to your audiobook or someone else's.

START DISTRIBUTING WIDE TODAY